Wind Tax Credits: 1992–2026 (never enough)

By Robert Bradley Jr. -- July 9, 2026Ed. Note: This repost is timely given the end of the Investment Tax Credit and the Production Tax Credit for unstarted wind and solar projects as of July 4, 2026, (One Big Beautiful Bill of 2025). For started (‘safe harbor’) projects, it is business-as-usual, which explains why the projects were started in the first place. If an unstarted project is completed by year-end (highly unlikely), it would also receive the ITC and PTC. Yesterday, the solar chronology was presented.

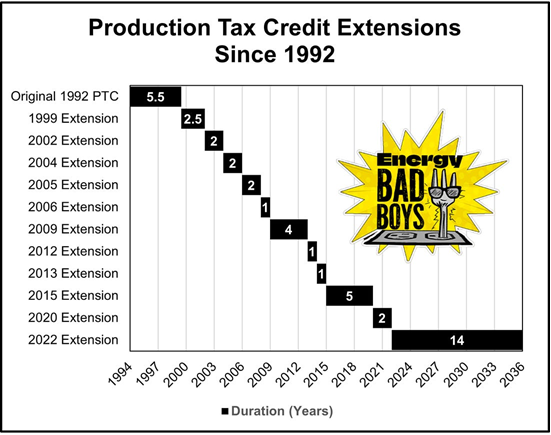

Wind power has relied on the Renewable Energy Production Tax Credit, first established in 1992. The PTC has been extended 12 times: 1999, 2002, 2004, 2005, 2006, 2008, 2009, 2013, 2014, 2015, 2018, and 2022 (IRA).

Source: Energy Bad Boys.

The 2008 extension is not mentioned in the above graph. The twelve extensions (add the 2022 Inflation Reduction Act) are noted here:

Renewable Electricity PTC Expirations and Extensions (Table 2, see Appendix below).

| Legislation | Date Enacted | PTC Eligibility Window | Lapse Before Extension? |

| Energy Policy Act of 1992 (P.L. 102-486) | 10/24/1992 | 1/1/1993-6/30/1999(closed-loop biomass)1/1/1994-6/30/1999 (wind) | — |

| Ticket to Work and Work Incentives Improvement Act of 1999 (P.L. 106-170) | 12/17/1999 | 7/1/1999-12/31/2001 | Yes7/1/1999-12/17/1999 |

| Job Creation and Worker Assistance Act (P.L. 107-147) | 3/9/2002 | 1/1/2002-12/31/2003 | Yes1/1/2002-3/9/2002 |

| Working Families and Tax Relief Act (P.L. 108-311) | 10/4/2004 | 1/1/2004-12/31/2005 | Yes1/1/2004-10/4/2004 |

| The Energy Policy Act of 2005 (P.L. 109-58) | 8/8/2005 | 1/1/2006-12/31/2007 | No |

| The Tax Relief and Health Care Act of 2006 (P.L. 109-432) | 12/20/2006 | 1/1/2008-12/31/2008 | No |

| The Emergency Economic Stabilization Act of 2008 (P.L. 110-343) | 10/3/2008 | 1/1/2009-12/31/201010/3/2008-12/31/2011 (marine and hydrokinetic)1/1/2009-12/31/2009 (wind) | No |

| The American Recovery and Reinvestment Act of 2009 (P.L. 111-5) | 2/17/2009 | 1/1/2011-12/31/20131/1/2010-12/31/2012 (wind) | No |

| The American Taxpayer Relief Act of 2012 (P.L. 112-240) | 1/2/2013 | 1/1/2013-12/31/2013 (wind) | Noa |

| Tax Increase Prevention Act of 2014 (P.L. 113-295) | 12/19/2014 | 1/1/2014-12/31/2014 | Yes1/1/2014-12/19/2014 |

| Consolidated Appropriations Act, 2016 (P.L. 114-113) | 12/18/2015 | 1/1/2015-12/31/20161/1/2015-12/31/2019 (wind)b | Yes1/1/2015-12/18/2015 |

| Bipartisan Budget Act of 2018 (P.L. 115-123) | 2/9/2018 | 1/1/2017-12/31/2017 | Yes1/1/2017-2/9/2018c |

| Further Consolidated Appropriations Act of 2020 (P.L. 116-94) | 12/20/2019 | 1/1/2018-12/31/2020d | Yes1/1/2018/-12/20/2019 |

Source: Information compiled by CRS using the Legislative Information System (LIS).

Infant Industry Not

Turning wind into electricity dates from 1888, when arc-lighting entrepreneur Charles F. Brush installed a windmill to power his Cleveland home. American companies would pick up the pace in the 1920s. During World War II, the 1.25 MW Grandpa’s Knob wind turbine distributed electricity to Central Vermont Public Service Corporation, an experiment that in 1945 led the Federal Power Commission (now FERC) to estimate the potential of domestic wind power.

Free energy spun the turbines, but the conversion to electricity was material- and capital-intensive—and intermittent. An 1883 article in Scientific American noted wind’s unpredictable flow, requiring “gathering it at the time when we do not need it and preserving it till we do.” But storage was—and still is—uneconomic.

For a full history of the not-infant wind power industry, see here and here.

Appendix: Full History of PTC Extensions

The PTC was first enacted in 1992 as part of the Energy Policy Act of 1992 (EPACT92; P.L. 102-486). Since 1999, the PTC has been extended 12 times (see Table 2). In many instances, the PTC lapsed before being reinstated. [Note: With the IRA of 2022, the PTC has been extended 13 times.]

When first enacted as part of the EPACT92, the PTC was available for electricity generated using wind or closed-loop biomass systems. The credit was initially set to expire on June 30, 1999. In addition to extending the PTC through December 31, 2001, the Ticket to Work and Work Incentives Improvement Act of 1999 (P.L. 106-170) added poultry waste as a qualifying technology. The PTC was again extended, through December 31, 2003, as part of the Job Creation and Worker Assistance Act (P.L. 107-147). The Working Families Tax Relief Act of 2004 (P.L. 108-311) included provisions extending the PTC through December 31, 2005.

Legislation enacted later in the 108th Congress substantially modified the PTC. The American Jobs Creation Act of 2004 (AJCA; P.L. 108-357) added new qualifying resources, including open-loop biomass (including agricultural livestock waste), geothermal energy, solar energy, small irrigation power, and municipal solid waste (landfill gas and trash combustion facilities). Instead of being able to claim the PTC for the first 10 years of production, these new qualifying resources were limited to a five-year PTC period. Further, open-loop biomass, small irrigation power, and municipal solid waste facilities had their credit amount reduced by one-half. The AJCA also introduced a PTC for refined coal, with a rate of $4.375 per ton (indexed for inflation after 1992), available for qualifying facilities placed in service before January 1, 2009.12

The PTC was extended twice during the 109th Congress. The Energy Policy Act of 2005 (EPACT05; P.L. 109-58) extended the PTC for all facilities except solar energy and refined coal for two years, through 2007. EPACT05 also added two new qualifying resources: hydropower and Indian coal. Hydropower was added as a half-credit qualifying resource. Indian coal could qualify for a credit over a seven-year period, with the credit amount set at $1.50 per ton for the first four years, and $2.00 per ton for the last three years, adjusted for inflation. EPACT05 also extended the credit period from 5 years to 10 years for all qualifying facilities (other than Indian coal) placed in service after August 8, 2005. The Tax Relief and Health Care Act of 2006 (P.L. 109-432) extended the PTC for one year, through 2008, for all qualifying facilities other than solar, refined coal, and Indian coal.

The PTC was again extended and modified as part of the Emergency Economic Stabilization Act of 2008 (EESA; P.L. 110-343). The PTC for wind and refined coal was extended for one year, through 2009, while the PTC for closed-loop biomass, open-loop biomass, geothermal energy, small irrigation power, municipal solid waste, and qualified hydropower was extended for two years, through 2010. Marine and hydrokinetic renewable energy were also added by EESA as qualifying resources. A new credit for steel industry fuel was also introduced. This credit was set at $2.00 per barrel-of-oil equivalent (adjusted for inflation with 1992 as the base year). For facilities that were producing steel industry fuel on or before October 1, 2008, the credit was available for fuel produced and sold between October 1, 2008, and January 1, 2010. For facilities placed in service after October 1, 2008, the credit was available for one year after the placed-in-service date or through December 31, 2009, whichever was later.

Table 2. Renewable Electricity PTC Expirations and Extensions

| Legislation | Date Enacted | PTC Eligibility Window | Lapse Before Extension? |

| Energy Policy Act of 1992 (P.L. 102-486) | 10/24/1992 | 1/1/1993-6/30/1999(closed-loop biomass)1/1/1994-6/30/1999 (wind) | — |

| Ticket to Work and Work Incentives Improvement Act of 1999 (P.L. 106-170) | 12/17/1999 | 7/1/1999-12/31/2001 | Yes7/1/1999-12/17/1999 |

| Job Creation and Worker Assistance Act (P.L. 107-147) | 3/9/2002 | 1/1/2002-12/31/2003 | Yes1/1/2002-3/9/2002 |

| Working Families and Tax Relief Act (P.L. 108-311) | 10/4/2004 | 1/1/2004-12/31/2005 | Yes1/1/2004-10/4/2004 |

| The Energy Policy Act of 2005 (P.L. 109-58) | 8/8/2005 | 1/1/2006-12/31/2007 | No |

| The Tax Relief and Health Care Act of 2006 (P.L. 109-432) | 12/20/2006 | 1/1/2008-12/31/2008 | No |

| The Emergency Economic Stabilization Act of 2008 (P.L. 110-343) | 10/3/2008 | 1/1/2009-12/31/201010/3/2008-12/31/2011 (marine and hydrokinetic)1/1/2009-12/31/2009 (wind) | No |

| The American Recovery and Reinvestment Act of 2009 (P.L. 111-5) | 2/17/2009 | 1/1/2011-12/31/20131/1/2010-12/31/2012 (wind) | No |

| The American Taxpayer Relief Act of 2012 (P.L. 112-240) | 1/2/2013 | 1/1/2013-12/31/2013 (wind) | Noa |

| Tax Increase Prevention Act of 2014 (P.L. 113-295) | 12/19/2014 | 1/1/2014-12/31/2014 | Yes1/1/2014-12/19/2014 |

| Consolidated Appropriations Act, 2016 (P.L. 114-113) | 12/18/2015 | 1/1/2015-12/31/20161/1/2015-12/31/2019 (wind)b | Yes1/1/2015-12/18/2015 |

| Bipartisan Budget Act of 2018 (P.L. 115-123) | 2/9/2018 | 1/1/2017-12/31/2017 | Yes1/1/2017-2/9/2018c |

| Further Consolidated Appropriations Act of 2020 (P.L. 116-94) | 12/20/2019 | 1/1/2018-12/31/2020d | Yes1/1/2018/-12/20/2019 |

Source: Information compiled by CRS using the Legislative Information System (LIS).

Notes: For all lapse periods, the PTC was retroactively extended. See text for full details on qualifying technologies during different time periods.

a. The PTC expired in January 1, 2013, before being extended on January 2, 2013.

b. For wind facilities beginning construction in 2017, the credit is reduced by 20%. The credit is reduced by 40% for facilities beginning construction in 2018, and reduced by 60% for facilities beginning construction in 2019.

c. The extension was fully retroactive, in that the extension only covered a time period prior to the extension’s date of enactment.

d. For wind facilities beginning construction in 2020, the credit is reduced by 40%.

The American Recovery and Reinvestment Act of 2009 (ARRA; P.L. 111-5) provided a longer-term extension of the PTC, extending the PTC for wind through 2012 and the PTC for other renewable energy technologies through 2013. Provisions enacted in ARRA also allowed PTC-eligible taxpayers to elect to receive a 30% investment tax credit (ITC) in lieu of the PTC. ARRA also introduced the Section 1603 grant program, which allowed PTC- and ITC-eligible taxpayers to receive a one-time payment from the Treasury in lieu of tax credits.13 Under ARRA, the Section 1603 grant program was available for property placed in service or for which construction started in 2009 or 2010. The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (P.L. 111-312) extended the Section 1603 grant program for one year, through 2011.

The PTC for wind, which was scheduled to expire at the end of 2012, was extended for one year, through 2013, as part of the American Taxpayer Relief Act (ATRA; P.L. 112-240). In addition to extending the PTC for wind, provisions in ATRA changed the credit expiration date from a placed-in-service deadline to a construction start date for all qualifying electricity-producing technologies. The PTC, as well as the ITC in lieu of PTC option, was retroactively extended through 2014 as part of the Tax Increase Prevention Act of 2014 (P.L. 113-295).

The Protecting Americans from Tax Hikes (PATH) Act of 2015, enacted as Division Q of the Consolidated Appropriations Act, 2016 (P.L. 114-113), extended the PTC expiration date for nonwind facilities for two years, through the end of 2016. The ITC in lieu of PTC option was also extended through 2016. For Indian coal facilities, the production credit was extended for two years, through 2016. Additionally, for Indian coal facilities, the placed-in-service limitation was removed, allowing the credit for production at facilities placed in service after December 31, 2008, to qualify.14 As part of Division P of the Consolidated Appropriations Act, 2016 (P.L. 114-113), the PTC for wind was extended through 2019. The credit was extended at current rates through 2016. For wind facilities beginning construction in 2017, the credit was reduced by 20%. The credit was reduced by 40% for facilities beginning construction in 2018, and reduced by 60% for facilities beginning construction in 2019.

The PTCs for nonwind technologies and the PTC for Indian coal expired at the end of 2016, but were retroactively extended for tax year 2017 in the Bipartisan Budget Act of 2018 (BBA18; P.L. 115-123). The PTC for technologies other than wind expired at the end of tax year 2017, and remained expired through 2018 and much of 2019.

The Further Consolidated Appropriations Act of 2020 (P.L. 116-94) retroactively extended the PTC for 2018 and 2019 for nonwind technologies, and extended the credits forward through 2020 for all technologies. P.L. 116-94 extended the PTC for wind facilities starting construction in 2020 at a rate of 60% of the full credit. The wind PTC remained at its previous phaseout rate of 40% of the full credit for facilities starting construction in 2019.