Headwinds for Offshore Wind (Rhode Island’s RFP a sign of trouble)

By Allen Brooks -- April 20, 2023“Why was there only one bid in response to Rhode Island Energy’s RFP if offshore wind is desirable (politically) and key to decarbonizing our economy? Was it because inflation and high-interest rates caused developers to hesitate over whether they could earn a reasonable profit?”

Last October, Rhode Island Governor Dan McKee announced a request for proposals (RFP) for offshore wind procurement in compliance with a new law. The law required the State’s primary utility company, Rhode Island Energy, to seek to contract up to 1,000 megawatts (MW) of new offshore wind generating capacity at market-competitive rates.

This offshore wind procurement has the potential to satisfy 30% of Rhode Island’s estimated 2030 electricity demand. When added to the 30-MW Block Island Wind farm and the contracted 400-MW Revolution Offshore Wind 1 project, the state will have secured about half of its projected energy needs from offshore wind.

Hype

At the time of the proposal, Interim State Energy Commissioner Chris Kearns stated: “With the release of the state’s largest offshore wind procurement RFP to date, Rhode Island is demonstrating our commitment to securing clean energy, reducing our dependence on natural gas, stabilizing long-term energy costs for consumers and capturing significant economic development and job benefits.”

He went on to say, “This is a major milestone in the progress toward achieving the nation-leading 100% Renewable Energy Standard by 2033, as well as the greenhouse gas emissions reduction goals in the Act on Climate.”

Reality

Last month, Rhode Island Energy announced it had received a single bid in response to the RFP. This was surprising given the Biden administration’s high-profile push for developing an offshore wind industry, releasing a plan to install 30 gigawatts (GW) of new offshore wind generating capacity by 2030 with another 15 GW of floating offshore wind being in the water by 2035. All to be accomplished while dramatically reducing the cost of the power produced….

Regarding other U.S. offshore wind projects, construction is underway in New England’s waters and will ramp sharply higher this summer. Two major wind farms – South Fork Wind and Vineyard Wind – with their towering turbines, will begin hammering the supporting foundations into the ocean floor this summer off Massachusetts, Rhode Island, and New York coasts.

The U.S. has two working offshore wind farms – Block Island Wind and Coastal Virginia Offshore Wind Pilot. The new wind farms will be larger and power many more homes and businesses than the operating wind farms. Those two wind farms have a combined total of 42 MW of wind-generating capacity utilizing seven turbines. The two new wind farms will have a combined 930 MW of generating capacity sitting atop 74 wind turbines, 43 of which are targeted for installation this summer.

The following maps show the respective locations of the South Fork Wind and Vineyard Wind projects. The maps demonstrate how much of the waters off Rhode Island and Massachusetts will be forever altered with the addition of these wind farms, which is just the start of the offshore wind build-out.

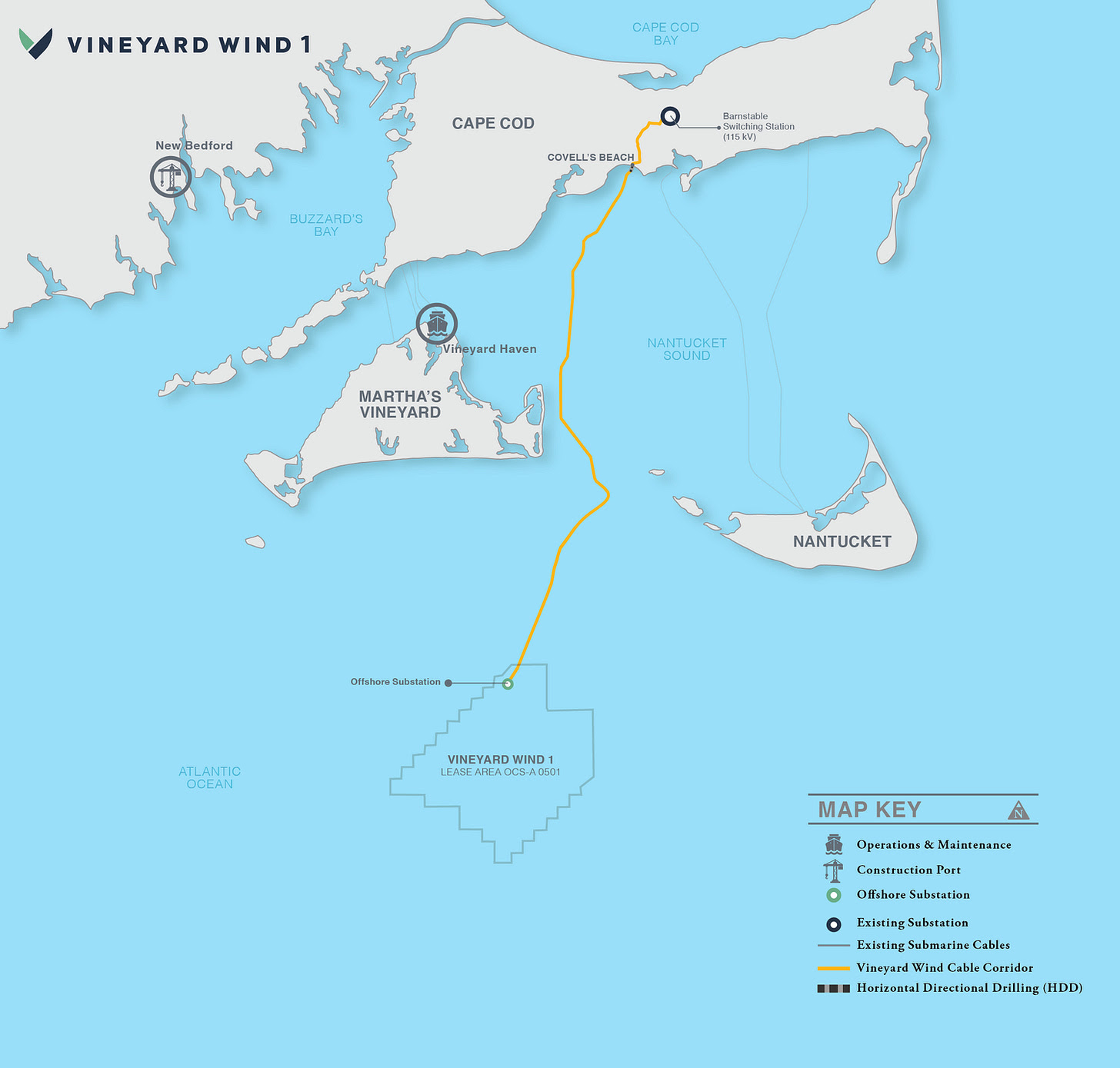

Exhibit 1. Vineyard Wind Lies South Of Martha’s Vineyard

Source: Vineyard Wind

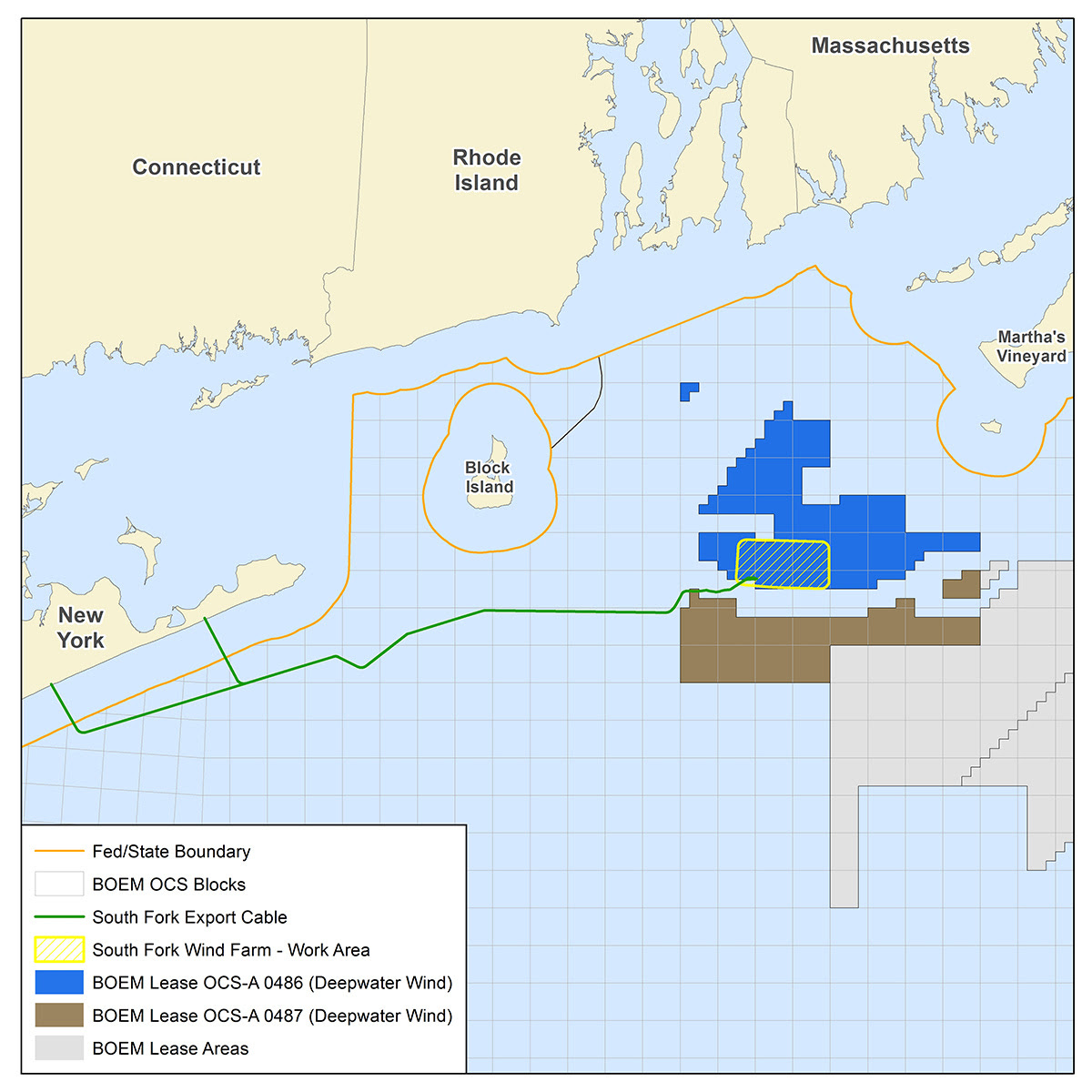

Exhibit 2. South Fork Wind Is Southeast Of Block Island

Source: South Fork Wind

The two wind farms will use different wind turbine designs provided by different manufacturers, although all the turbines will be built in Europe because the U.S. does not have a local supplier. To capitalize on the stronger offshore winds at higher elevations, the turbines will be much taller than onshore wind turbines.

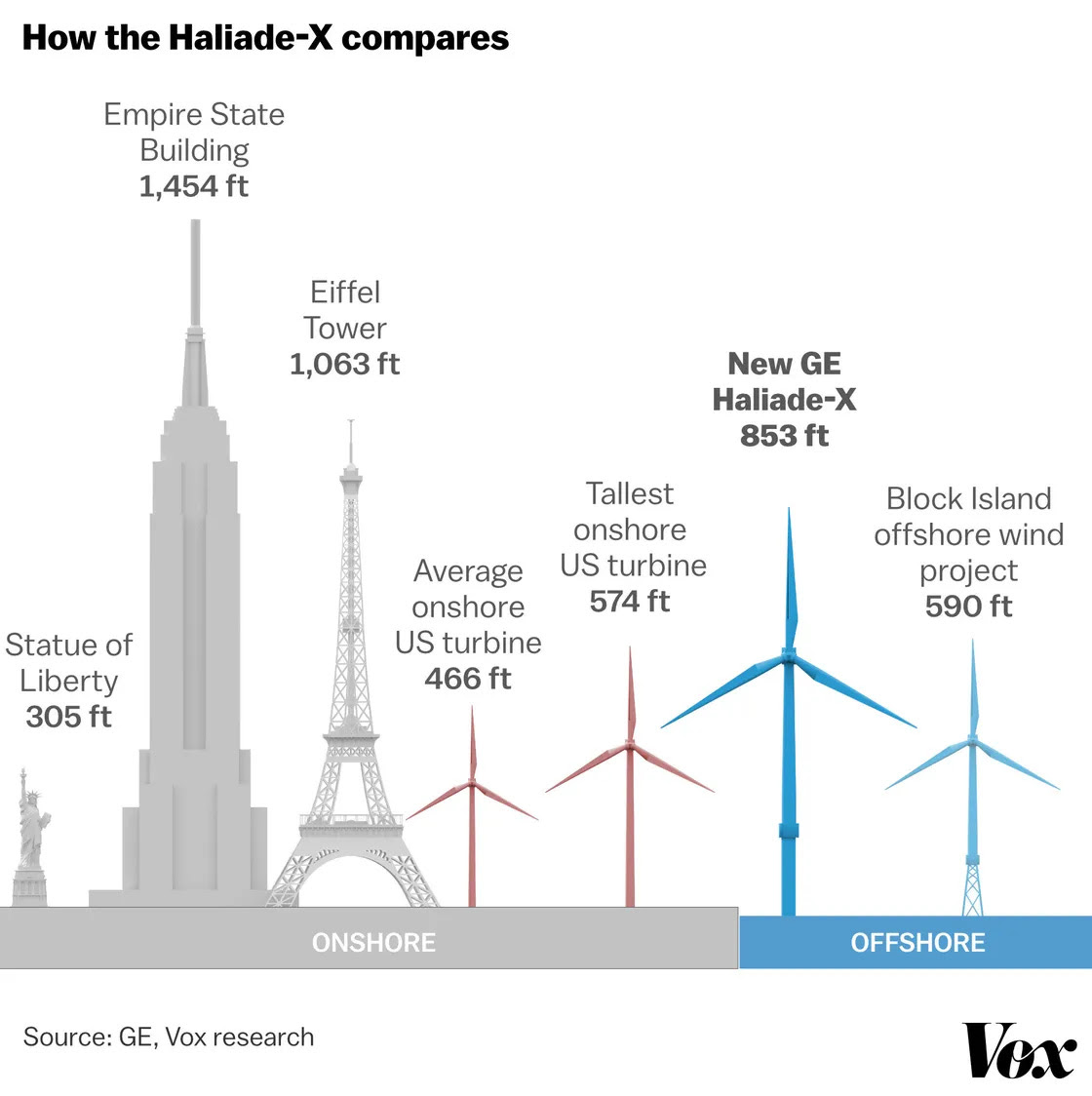

The following chart shows the height of a typical onshore wind turbine, the height of the tallest one, and the height of the new General Electric Haliade-X offshore wind turbines, which will be utilized by Vineyard Wind. For comparison, the chart also shows the height of the Block Island Wind turbines, the first U.S. offshore wind farm installed in 2016. The South Fork Wind Farm plans to use an 11-MW Siemens Gamesa turbine, whose dimensions place it between the Block Island Wind and the Haliade-X turbines. By including sketches of popular landmarks, readers may more easily relate to the scale of these new offshore wind turbines. It also explains why coastal residents want the turbines located farther offshore, hopefully over the horizon where they will not be visible from shore.

Exhibit 3. Offshore Turbines Are Growing Larger

Source: GE, Vox

With its nearly 900-foot height and 350-foot rotor blades, the length of a football field, the new Haliade-X turbine is projected to have a capacity factor of 63%, which is higher than existing offshore wind turbine models that generally have capacity factors around 45%. Larger wind turbines are key to improving the economics of offshore wind farms, but they are unproven and require even larger areas.

The capacity factor of an electricity-producing power source is a key input for calculating the “levelized cost of energy” (LCOE). That is because the LCOE of an energy-generating asset can be thought of as the average total cost of building and operating the asset per unit of total electricity generated over an assumed lifetime. By utilizing higher capacity factors – 50+% versus 45% – the projected cost of electricity can be reduced making that energy source cheaper than alternatives. This is important in the current environment of rising raw material costs and higher interest rates impacting renewables’ cost of capital.

Proponents of offshore wind point to a future when wind energy reaches 65-85% utilization, appearing to offer the prospect of supplying all the electricity needed for the economy from renewable energy. However, the high utilization factors exist for brief periods and are never sustained. Thermal plants (fossil fueled, nuclear) consistently generating high utilization rates because they can deliver their power constantly, except when they need maintenance, repair, or refueling.

Rhode Island Energy’s RFP

Why was there only one bid in response to Rhode Island Energy’s RFP if offshore wind is desirable (politically) and key to decarbonizing our economy. Was it because inflation and high-interest rates caused developers to hesitate over whether they could earn a reasonable profit? This issue has moved front and center: CEOs of two major European oil companies in the renewables rush, especially wind, pulled back because of the poor returns of projects.

Moreover, Shell’s CEO stated his company will not use the profits from its fossil fuel businesses to subsidize renewable energy projects. Shell’s renewable business is a partner in an East Coast offshore wind farm development and has indicated it is having profitability issues but will continue with the project. That decision may have been caused by the Massachusetts Public Utility Commission’s approval of utility Power Purchase Agreements over developer Avangrid Renewables’ objections. It argued the project is “unfinanceable at current prices.”

The single response to the Rhode Island Energy RPF came from the partnership of Danish wind developer Ørstad, who owns the Block Island Wind farm, and New England utility Eversource, who previously partnered with Revolution Wind 1. Revolution Wind 1 is contracted to provide 400 MW of the wind farm’s 704 MW of capacity to Rhode Island Energy. The Ørstad partnership offered 844 MW of power from Revolution Wind 2 to be developed adjacent to Revolution Wind 1. Terms of the proposal have not been made public and are not expected to be disclosed until June.

Dave Bonenberger, president of Rhode Island Energy, said in a statement: “Although we had hoped to see more developers put forward additional proposals within this appeal, we also know there are a multitude of factors at play right now.” He did not enumerate the issues, but he went on to say: “As we move forward, our evaluation will consider future energy affordability and how this proposal meets the requirements of both the RFP and state law.”

Examining the Fine Print …

I recently obtained a copy of the JOINT DEVELOPMENT AGREEMENT [JDA] BETWEEN THE STATE OF RHODE ISLAND AND DEEPWATER WIND RHODE ISLAND, LLC. Deepwater Wind (DWW) developed the Block Island Wind farm, which started operating at the end of 2016. It was sold to Ørstad in 2018 for $510 million. The project had an estimated cost of $300. The JDA may contain clues as to why only one proposal was submitted and that from an Ørstad partnership.

Under the Definitions section of the JDA are the following details:

T. Phase I of the Project (“Phase I”) – A wind power project to be located in state waters having approximately twenty (20) MWs of nameplate capacity and interconnected to both the electric power systems of BIPCO [Block Island Power Company] and mainland Rhode Island.

U. Phase II of the Project (“Phase II”) – A wind power project to be located within the SAMP [Special Area Management Plan] area in United States waters off of the coast of Rhode Island having approximately three hundred eighty-five (385) MWs of nameplate capacity and interconnected to the electric power systems of mainland Rhode Island, and which, in the event Phase I is Discontinued, is also interconnected to the electric power system of BIPCO.

According to the language above, DWW, now Ørstad, has a monopoly on offshore wind power development for Rhode Island until the company has built a project with at least 385 MW of power. What does this agreement mean for power pricing? Was Rhode Island Energy unaware of the terms of this agreement between Ørstad and the state, or was the company thinking that because the 400 MW of Revolution Wind 1 had been contracted the monopoly was ended? Maybe the bigger question is whether the unsettled economics of offshore wind as demonstrated by Avangrid Renewables’ effort to seek adjustments to power contracts already signed has developers wary of making proposals.

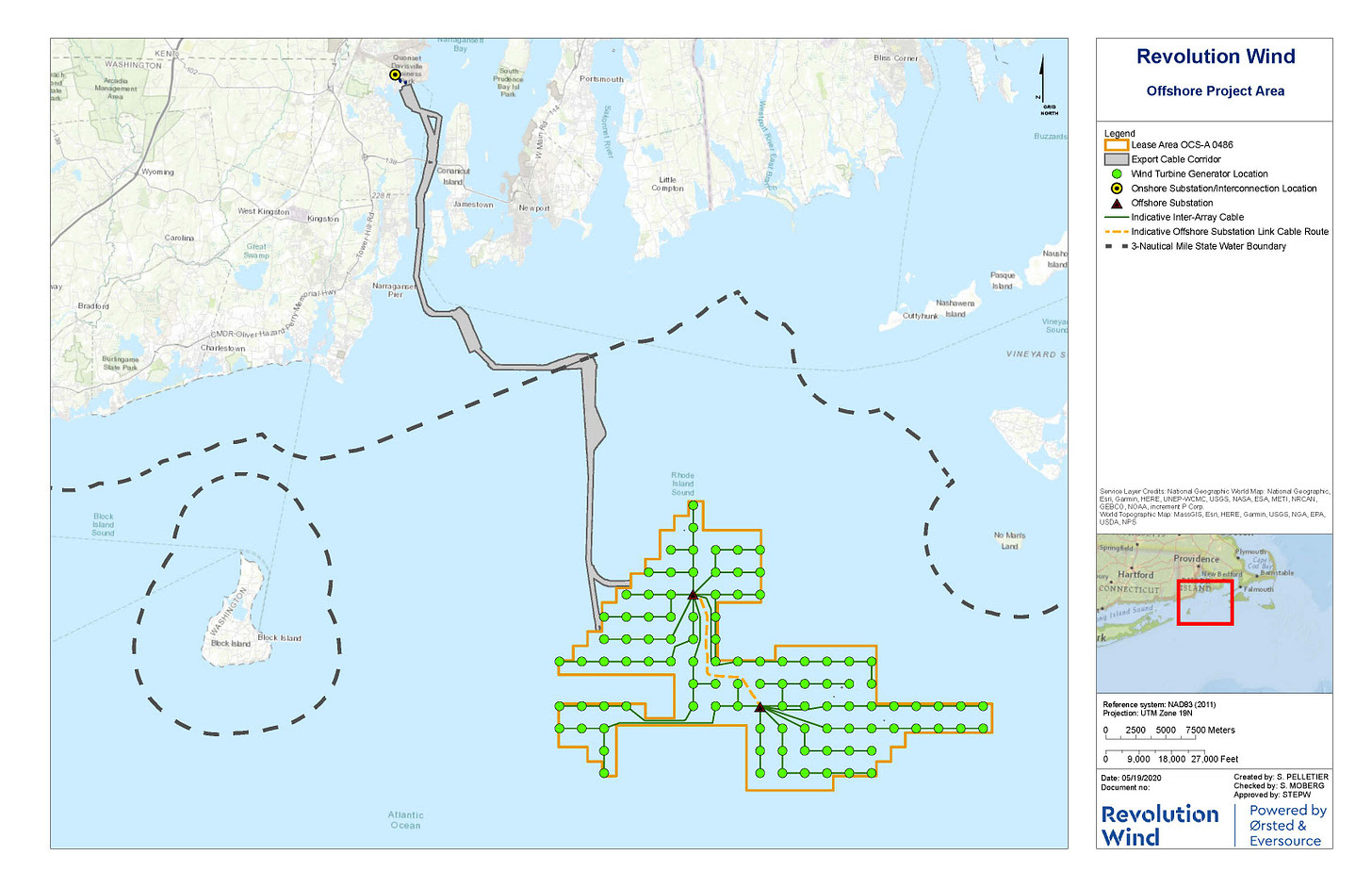

National Grid, the predecessor to Rhode Island Energy, invested in the installation of a submarine cable between Block Island and the Rhode Island mainland to transport surplus power from the Block Island Wind farm, while also allowing possible shipment of electricity to the island if needed. As the map below shows, the location of Ørstad’s Revolution Wind 1 and 2 projects allows for power cables to easily connect with Block Island and its submarine power cable to shore.

Exhibit 4. Revolution Wind Strategically Located Near Block Island

Source: Revolution Wind

Until June when Rhode Island Energy will disclose the details of the Revolution Wind 2 bid, we have no idea what electricity price the developers seek. How will the price be evaluated? One likelihood is that the price will not matter as the utility is under a mandate to contract offshore wind power. This outcome is based on the history of Block Island Wind’s power price evaluation by the Rhode Island Public Utility Commission (PUC). After the PUC rejected the initial submission, the Rhode Island legislature rewrote the rules that allowed for evaluating the economics of offshore wind projects.

No longer can the PUC perform a “cost/benefit” analysis. Thus, Block Island paid over 24 cents per kilowatt-hour with a guaranteed 3.5% annual price increase for the 20-year life of the contract for the wind farm’s power when electricity onshore was priced at a quarter to half the price. Because Block Island’s electricity was very expensive from diesel generation, the high electricity price still represented a discount.

Ørsted and Eversource continue saying Revolution Wind 1’s construction is expected to begin later this year and “be operational in 2025.” The problem is the project has yet to receive its final Environmental Impact Statement (EIS) from the Bureau of Ocean Energy Management (BOEM). When the draft EIS was exposed for public comment, there were 123 comments and objections. Included in the comments and objections were ones from fishery management councils, the Rhode Island Department of Environmental Management, and NOAA Fisheries. They were all suggesting changes or enhancements to the project. The final EIS will trigger additional review by the Rhode Island Coastal Resource Management Council and potentially generate lawsuits from objectors and commentators who feel the changes mandated by the final EIS are insufficient.

Since Revolution Wind 1 was proposed in 2020, wind turbine manufacturers have reduced their capacity due to the hundreds of millions of dollars of losses they have incurred as raw material inflation has overwhelmed the contracted prices for wind turbines. These challenges have not been fully corrected. Additionally, issues with increasing whale deaths could slow or derail projects despite government agencies claiming there is no linkage between offshore wind activity and a rise in whale deaths. (A topic for another article.)

Is it still realistic to think Revolution Wind 1’s timetable can be maintained? With each delay, the construction timeline will begin to possibly interfere with the work schedules of other offshore wind projects and the availability of installation vessels. Every delay impacts offshore wind farm construction costs and squeezes profit margins. Could we see more developers seeking rate relief given the sharply rising costs? Or is the Rhode Island RFP single bid a sign that despite clean energy mandates, few offshore wind developers will bid on projects, helping support higher prices for the winning bidders? In either case, more expensive offshore wind will drive average electricity prices higher. How many Rhode Islanders understand that reality?