Betting the House on Plant Vogtle

By Joseph Pokalsky -- September 18, 2018

[Editor Note: The touted nuclear power renaissance in the United States has been stymied by engineering, procurement, and construction problems with new-generation plants, namely Westinghouse’s AP1000 design. With yet another recently announced cost overrun, two minority owners of Plant Vogtle III and IV must soon decide on whether to continue with their investment with another ante-up for what was originally estimated to cost $14.3 billion (with a four-year construction period) that is now estimated by the majority owner to cost $25 billion with years still to run.

The author below reports on the latest developments for the two Vogtle Units and provides the framework for an unbiased, probability-based model that can be used by the minority owners to support their upcoming decision on the project.]

“The reluctance to cancel this project stems from the fact that so much has been expended to date. Regardless of how much they have vested, the minority owners need to acknowledge that Vogtle has fallen victim to the sunk cost fallacy and they need to objectively evaluate the costs and risks of their alternatives at the margin.”

On or before September 30, the two minority owners of Plant Vogtle Units 3&4, Oglethorpe Power Corporation (OPC) and Municipal Electric Authority of Georgia (MEAG), will decide if they want to assume their portion of the recently announced $2.3 Billion cost overrun and continue participating in the project plagued by multiple delays and cost overruns that have increased rates, impaired balance sheets, and strained borrowing capacities. They will decide if they want to ante-up and bet the house on flawless going-forward project execution at Vogtle.

I would advise them against that bet, and I’m in good company. This past February, the day after he left his position as Chairman of the GA Public Service Commission (PSC), Stan Wise was asked in a radio interview if GA Power would meet the revised project schedule that was hastily approved by the PSC last December. He replied, “I wouldn’t bet my house on it.”

In only six months Stan Wise would be proven correct, along with the PSC staff and industry experts that voiced concerns about the project during December’s hearings for the Seventeenth Semi-Annual Vogtle Construction Monitoring (VCM). Many of these concerns focused on Southern Nuclear’s ability to assume the responsibility of the primary contractor and effectively manage, within their proposed budget revision, a cost-plus contract for continuing Vogtle after Georgia Power terminated its fixed price Engineering, Procurement, and Construction Agreement (EPC) with Westinghouse.[1]

Unpleasant Truths

To support their request to the PSC for approval of the budget revision needed to move forward with the project, GA Power’s consultant PricewaterhouseCooper (PwC) prepared a Quantitative Risk Assessment (QRA). The conclusion of the assessment was that under Southern’s management the going forward risks for the project would be nowhere near what was realized when it was managed by Westinghouse.

In their testimony however, the PwC representative stated that they did not validate the inputs for the analysis they received from Southern, would not Rep and Warrant the results of the QRA, and stated that certain risks were omitted from the analysis despite the fact they could potentially have a large impact on the project cost and timeline.[2]

On behalf of a ratepayer advocacy group, I reviewed the QRA and determined that the foundation of the analysis was what is literally called “the lack of knowledge distribution.” The inputs for this risk review were not derived from statistical analysis of prior project results, but were determined independently by those at Southern involved in structuring the analysis.

In my testimony, I informed the Commission that the results of the QRA were very much different than one would expect given the history of the project; that commonly used risk assessments such as scenario analysis would produce very different results; and that more robust project risk assessment methodologies should have been used. More importantly, I explained to the Commission that 95% of the results were determined by only six data points and an admittedly made up correlation coefficient that could be adjusted to influence the outcome.

The recent cost overruns have demonstrated that the budget risks outlined in the QRA are extremely unreliable. My interpretation of the QRA assigns a 1 in 5 chance of the recently announced cost overrun occurring over the remaining five year life of the project, and that the chance that the overrun would occur as it did this August was 1 in 15. The reaction of rating agencies and the need of the project owners to recapitalize their balance sheets indicates to me they had similar expectations.

Moodys recently downgraded Georgia Power, citing the size of the recent cost overrun occurring so soon after the budget revision of last December. Guggenheim Securities’ research department recently noted regarding Vogtle; “we aren’t comfortable assuming that further cost increases and the equity overhang will not continue.”

OPC budgeted in 2017 what they deemed a conservative $490 MM contingency for future cost overruns in its share of the project. OPC’s share of the recent $2.3 B overrun, is $690 MM, $200 MM more than the currently budgeted contingency. Fitch Ratings recently placed $3.9 B of OPC debt obligations on Rating Watch Negative and OPC is evaluating means to replenish the Vogtle contingency for additional cost overruns. It estimates that the operating budget could increase by 5% to 6%. Assume that ratepayers from the OPC Member EMCs will pick up the tab.

Fitch Ratings also recently placed $5.17 B of MEAG’s bonds on Rating Watch Negative. MEAG entered into a twenty-year sale agreement with Jacksonville Electric Authority (JEA) for a portion of its ownership. JEA’s attorney hired Navigant Consulting to perform an Independent Economic Analysis for its share of Vogtle and now wants to terminate that agreement. On August 17th JEA sent a letter to MEAG’s CEO James Fuller stating,

Any vote to continue this project ignores well-documented facts and is contrary not only to the interests of JEA and its constituents, but also to the interests of MEAG’s own constituents and their ratepayers.

Last week JEA filed a lawsuit in Florida seeking to have the contract voided and MEAG filed a lawsuit in the Northern District of Georgia claiming that JEA is trying to renege on a 2008 agreement to purchase power from them.

Sunk Cost Fallacy, Cronyism, and the ‘Second Coming’

The reluctance to cancel this project stems from the fact that so much has been expended to date. Regardless of how much they have vested, the minority owners need to acknowledge that Vogtle has fallen victim to the sunk cost fallacy and they need to objectively evaluate the costs and risks of their alternatives at the margin.

In my testimony to the PSC I presented a benchmark analysis for the marginal cost to complete Vogtle and showed that it was approximately five times that for a natural gas fired baseload plant. The recent overrun equates to $1 MM per MW of generation capacity, and by itself is more than it would cost for a much less risky construction of a natural gas fired plant.

PSC staff, industry experts, and I also presented to the PSC additional analysis such as Levelized Cost of Energy (LCOE), and Present Value Analysis for combinations of gas plants, renewables, storage, and efficiency that also provided compelling reasons for terminating the project. This analysis was very much aligned with the results summarized in Navigant’s “Independent Economic Analysis” prepared for JEA last September.

Still, the PSC ignored its own staff and outside experts and sided with GA Power approving the budget revision. During the period of the 17th VCM hearings, PSC Commissioners made public statements regarding project benefits of job creation, tax revenues, domestic energy security, an unsubstantiated $15 per MMBtu price forecast for natural gas, as well as a reference to the Second Coming to defend their position; anything but collectively analyzing the costs and risks of Vogtle versus other alternatives in order to uphold their responsibility to ratepayers for low cost, reliable energy.

Playing the Odds

So that’s the hand that’s been dealt to the minority owners. How do they decide whether or not to continue on with Vogtle? Quantitative assessments for Plant Vogtle such as PwC’s QRA have been proven to be as woefully inadequate. There are too many unknowns for a project such as this where engineers, management, and contractors are learning on the job. Their persistence is admirable, but is likely not in the best interest of ratepayers.

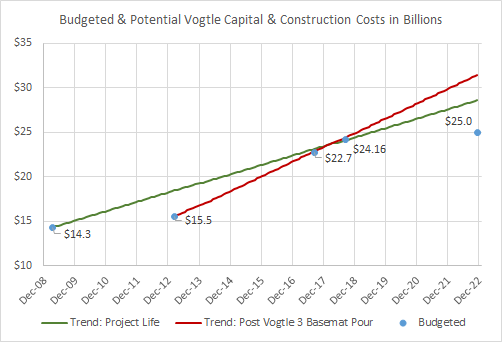

Below is a graph that tracks the numerous budget revisions to Vogtle over time as well as extrapolates two cost paths based upon these revisions to the currently expected project completion date.

The reason for the two cost path trajectories is to separate the periods used to estimate potential final costs between the one prior to and the one after construction began on the project. These extrapolations result in a range of final project costs between $28.5 and $31.5 B. Vogtle proponents may criticize the accuracy of these extrapolations, but they aren’t required to be perfect in order to support the decision making process I outline below. Regardless, the graph clearly shows that the current expectation for completing the project for a total of $25 B is substantially below both trends and it’s an important point to consider.

Only after the fact will perfect information be available to validate a choice to abandon Vogtle and pursue other options. But, if continuing on with the project and suffering additional cost overruns, it will be too late to protect ratepayer interests. An analogy is the decision making process for evacuating prior to a potential natural disaster. Once the information needed to verify that not evacuating will result in dire consequences, it is too late.

My opinion is that the decision on Vogtle can be boiled down to the joint probability of potential outcomes for the two drivers of the absolute and comparative valuations of Vogtle.[3]

The first driver is potential additional Vogtle cost overruns and how they would impact ratepayers. For example, if these final project costs from the extrapolations are realized, OPC’s share would range from $8.55 to $9.45 B. Recent public statements from OPC state that given the most recent final cost forecast of $25 B, its operating budget will increase by around 5.5%.

Using the same benchmark comparisons, if the final project costs range between $28.5 and 31.5 B, OPC will require an increase in their operating budget between 8.5% and 15.5%, in addition to the stated 5.5%. To protect ratepayer interests from further rate increases, there have to be assurances that the final costs won’t exceed $25 B. GA Power management enumerated a long list of issues that can cause further cost overruns in its filing for the 18th VCM.[4]

The second driver is future natural gas prices. GA Power has stubbornly clung to a very high natural gas price forecast like that used to support the original approval for Vogtle in 2009[5], before our domestic Shale Revolution that drove prices down from $14.87 in June 2008 to $2.875 in June 2018. In my opinion, this is the primary reason for the large divergence between project valuations from PSC staff and industry experts versus GA Power, and a reason PSC Commissioner Echols admitted last December that Vogtle was an uneconomic option for ratepayers versus a natural gas fired plant.

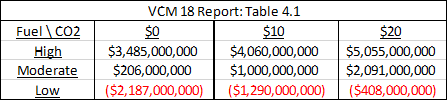

To support continuing on with Vogtle, it has to be a more economical option than a natural gas plant. That is, natural gas prices must return to their pre Shale Revolution era prices and possibly higher. Given that $15 per MMBtu was bantered about during the 17th VCM, I’ll refer to it as the $15 per MMBtu Case. The Table and the quote below is from the GA Power’s 18th VCM Report and was used to defend its position that Vogtle is the most economical option for ratepayers.

Positive number means the Project is less costly than the gas-fired CC alternative.

“The weighted average expected value of the relative savings for completion of the Project as compared to the gas-fired CC alternative is $1.3 billion based upon the results provided in Table 4.1.” [6]

Given the analysis I’ve reviewed, GA Power’s Natural Gas Price Forecasts are indicated to be much higher than those from industry experts. GA Power does not publically report its forecast, forecast methodology, or weighted average valuation methodology.

I personally think that there will be more cost overruns at Vogtle and that the $15 per MMBtu Case will never be realized. [7]. But that doesn’t necessarily matter in deciding whether or not to cancel the project.

As outlined earlier, avoiding further rate increases requires that Vogtle doesn’t exceed the recently revised budget of $25 B. In addition, to assure that Vogtle is in the most economic option, the $15 per MMBtu Case needs to be realized.

Therefore, for continuing on with Vogtle turning out to be in the best interest of ratepayers it requires that:

- Final project costs won’t exceed $25 B, AND the $15 per MMBtu Case is realized.

For canceling Vogtle to turn out to be in the best interest of ratepayers it requires that:

- Final project costs won’t exceed $25 B, AND the $15 per MMBtu Case is not realized.

- Final project costs will exceed $25 B, AND the $15 per MMBtu Case is not realized.

- Final project costs will exceed $25 B, AND the $15 per MMBtu Case is realized.

Conclusion

Assigning an equal probability, or 50/50, to each of the possible, uncorrelated outcomes, results in a 25% chance that continuing on with Vogtle will turn out to be in the best interest of ratepayers, and a 75% chance that canceling Vogtle will turn out to be in the best interest of ratepayers.

Biasing probabilities for one’s expectations changes the results. For example, assigning a 65 % probability to further cost overruns at Vogtle and a 30% probability that the $15 per MMBtu Case is realized, results in a 10% chance that continuing on with Vogtle will turn out to be in the best interest of ratepayers, and a 90% chance that canceling Voglte will turn out to be in the best interest of ratepayers.

If the minority owners can negotiate a price cap on the shared project costs to be $25 B, and they assign a 30% probability that the $15 per MMBtu Case is realized, then there is a 30% chance that continuing on with Vogtle will turn out to be in the best interest of ratepayers, and a 70% chance that canceling Voglte will turn out to be in the best interest of ratepayers.

Additionally, if considering renewables in the alternative generation mix for Voglte, the potential impact of the $15 per MMBtu Case natural gas will be less and the expected probabilities can be adjusted to reflect this as well as for potential hedging of gas price exposures.

To me the answer is obvious. Regardless of one’s expectations, Vogtle should be canceled.

OPC and MEAG don’t have to agree with my analysis, but they should heed Stan Wise.

Don’t bet your house on Plant Vogtle.

————

[1] There were other concerns expressed, including whether the revised budget itself was in ratepayer interests, and if there was actually a need for the Vogtle capacity. More details of the circumstances surrounding and concerns expressed at the 17th VCM Proceedings can be found here.

[2] Ibid.

[3] This comparison is very simplistic and ignores other alternative capacity options such as renewables, but it’s the comparison used by GA Power to support completing Vogtle in section “4. An updated comparison of the economics of the certified project to other capacity options” in its Semi-annual Vogtle Construction Monitoring Reports.

[4] Eighteenth Semi-annual Vogtle Construction Monitoring Report, February 28 2018, Docket No. 29849, p.7

[5] GA Power has also stubbornly clung to a same vintage load forecast that according to expert testimony overestimated its capacity requirements in 2016 by 5 times their share in the new Vogtle units.

[6] Eighteenth Semi-annual Vogtle Construction Monitoring Report, February 28 2018, Docket No. 29849, Table 4.1, p. 34.

[7] Additionally, if pursuing a gas plant option, OPC Member EMCs can hedge their gas price exposure. Renewables won’t require a fuel price hedge.

—————–

Joseph Pokalsky, Managing Director of Prosumers Energy, has more than 25 years of experience in the energy and utility sector. He helped found Southern Company Energy Trading and Marketing; provided services for resource planning, production costing, and power procurement for a group of EMCs in the Oglethorpe System that opted not to participate in the Vogtle project; and was a Director specializing in Risk Management for PwC’s Energy and Utility Practice.

Mr. Pokalsky is a Chartered Financial Analyst and received Masters in Finance and City and Regional Planning from the University of Pennsylvania.

[…] https://www.masterresource.org/georgia-power-plant-vogtle/vogtle-more-problems/ […]

Mr. Pokalsky, I have worked extensively as an engineer at several nuclear power stations. can you provide a resource that details the technical problems besetting the project? I almost took a job at Vogtle last year.

I am a nuclear engineer that worked on the nearly identical VC Summer project in SC that was cancelled last year. So my observations may be biased.

I believe that our government is engaged in an effort to keep NG prices down in order to starve Russia of foreign earnings. This strategy was also used in the 1980s against the USSR.

Part of this strategy is to wean other nations away from from buying Russian NG by exporting US LNG.

I plead agnostic on the perils of “fracking”. It does appear to rapidly deplete wells. I wonder how long we can maintain a drilling pace that that outruns well depletion that remains economical.

Low NG prices are what make apparently “cheap” renewables feasible.

Legacy nuclear power stations are being closed because they cannot compete with NG under current prices and renewable energy policies. Because of the skilled nature of the workforce required to operate these plants and other regulatory requirements, they cannot simply be mothballed for a few years and then easily started back up. TVA did this but they are a federal agency.

At some point, probably within 5 years, our LNG exports will take off at the time when many nuclear power stations will have been closed and NG well depletion might be significant.

So I am not so sure that NG prices won’t return to historic norms or perhaps go to the high end.

With regards to the AP1000 reactor:

One major problem was Westinghouse’s poor selection of suppliers for the domestic projects in GA and SC. The Chinese projects used different suppliers.

The US no longer has the workforce to build these plants. Many of the welders, carpenters, electricians were in their 50s and older. Even after Summer was cancelled I read that Vogtle still has this problem.

The plant design was not fully complete when construction started.

Two of the Chinese AP1000 projects are now on-line and had very successful startup tests. For some reason, although they too were completed behind schedule, any lessons learned did not prevent the problems experienced in the US. Perhaps this is be ause of the supply and workforce problems specific to the US noted above. Interestingly, the Chinese have scaled up the AP1000 design for future deployment.

Unless we experience a significant drop in electric power demand, most likely due to a dramatically slowed economy, we have a good chance of having an electricity shortage in the medium term future.

[…] announced a $3.7 billion loan guarantee for two nuclear reactors being built by Southern Co. Plant Vogtle, the only nuclear facility under construction in the U.S has been beset by engineering, […]