The Baltic Eagle Gas Hub (US-to-EU LNG to the Rescue)

By Robert Bradley Jr. -- June 30, 2026Ed. Note: This post reproduces an advertisement in the Wall Street Journal (April 30, 2026) by central European energy company Orlen, titled “The Baltic Eagle Gas Hub Is Emerging as Europe’s Energy Firewall.” It documents how changed prices and profit opportunities have and will demote the Strait of Hormuz for petroleum and LNG transportation “as if led by an invisible hand”.

“By linking regional markets with global ones, the Baltic Eagle Gas Hub is emerging as part of a new energy-security architecture in Europe—one based not only on diversification of supply, but also on flexibility, regional cooperation, and the ability to respond quickly to shifts in the global environment.”

Rising geopolitical tensions are rippling through global energy markets, with fuel supplies increasingly used as instruments of influence. Countries are responding by diversifying where they buy energy to reduce dependence on any single source. In Central and Eastern Europe (CCE region), U.S. LNG and the developing Baltic Eagle Gas Hub are beginning to anchor that shift.

Energy security has moved to the foreground. Once defined largely by price and reliability, it now turns on resilience to geopolitical disruption and control over critical infrastructure. Natural gas has long been part of that equation—and at times a tool of political pressure. In Europe, that dynamic was most visible in Russia’s role as the continent’s main supplier before its invasion of Ukraine. The CEE region, shaped by history, remained structurally dependent on Moscow for decades.

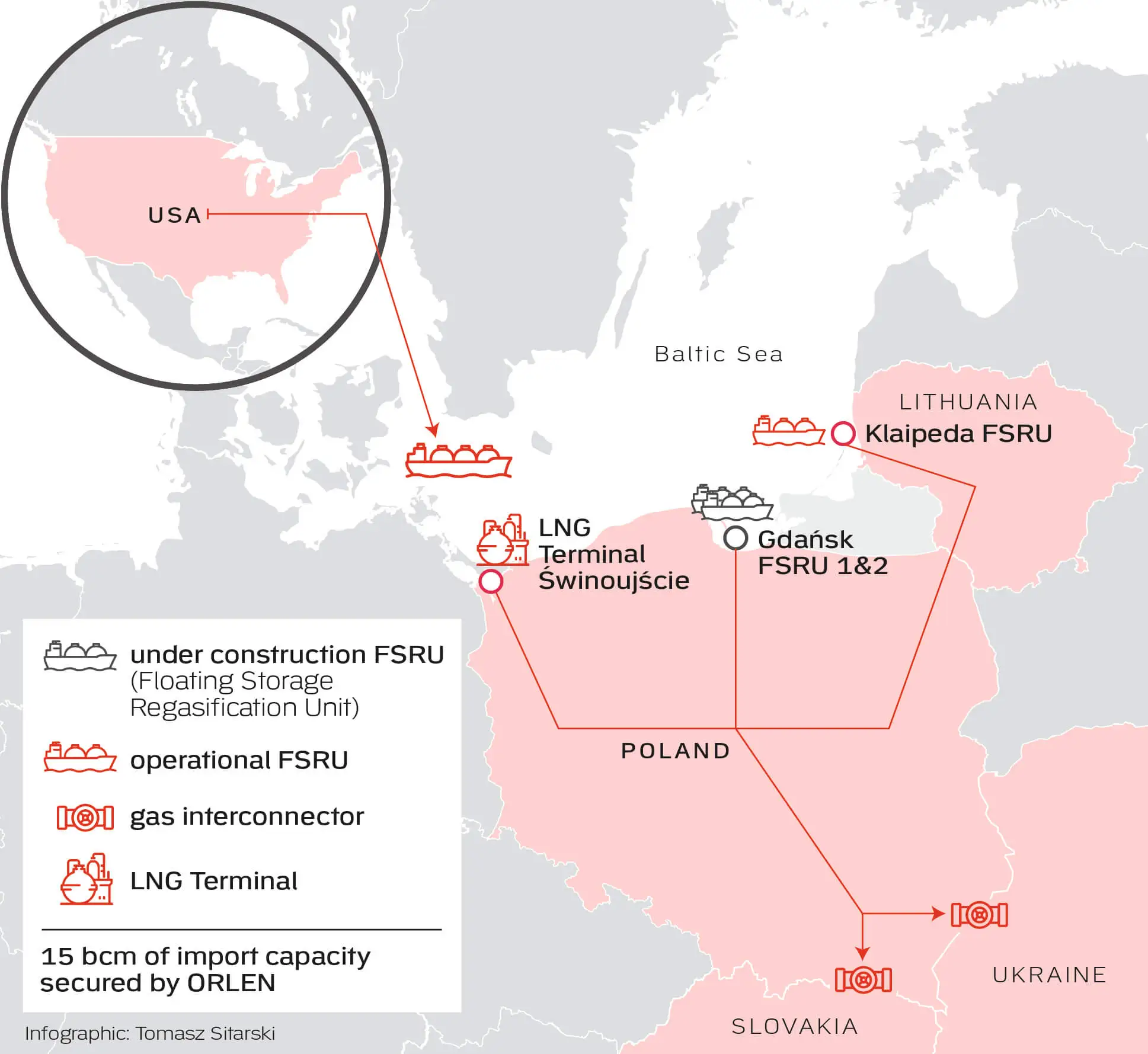

Access to diversified gas supplies, storage capacity, and cross-border interconnectors now defines how resilient a system is. Together, these elements give transmission networks flexibility and allow countries in the region to respond more effectively to supply shocks, limiting external pressure. Poland moved early to build that flexibility. It developed the subsea Baltic Pipe, linking gas fields on the Norwegian continental shelf with its domestic network, and expanded the LNG terminal in Świnoujście, which now has regasification capacity of 8.3 billion cubic meters a year.

A floating terminal (FSRU) near Gdańsk, with capacity of 6.1 billion cubic meters annually, is under construction, and a second unit with potential capacity of 4.5 billion cubic meters is under consideration. Poland has also expanded cross-border links with neighboring countries, increasing the number of routes through which gas can flow.

Poland’s gas consumption stands at close to 20 billion cubic meters a year and could rise by as much as 10 billion cubic meters over the next five-to-six years. ORLEN is the main supplier to the domestic market while also exporting gas across the region.

The company is expanding production, primarily in Norway and Poland, where it currently produces about 8 billion cubic meters. Over that period, the EU has significantly reduced its dependence on Russian hydrocarbons.

According to the European Commission, the EU imported about 290 billion cubic meters of gas in 2025, including 140 billion cubic meters of LNG. The United States accounted for nearly 58% of LNG imports. Poland is among the countries relying on that supply. In 2025, 62 cargoes from the U.S. were delivered to the Świnoujście terminal. Qatar ranked second, with 17 deliveries, while smaller volumes came from Trinidad and Tobago and a terminal on the border of Senegal and Mauritania.

These flows underscore the importance of U.S. gas for the region. Energy ties between the U.S. and Europe now extend beyond trade, strengthening economic and political links while reducing exposure to supply pressure.

Building the Baltic Eagle Gas Hub

ORLEN is developing the Baltic Eagle Gas Hub to serve gas demand across Central and Eastern Europe, including in countries without direct access to maritime routes. The hub rests on a combination of infrastructure: the Baltic Pipe bringing gas from the north, the Świnoujście terminal, the future FSRU in Gdańsk and a network of cross-border interconnectors.

The company has also secured capacity at the Klaipėda terminal, with regasified LNG transported to Poland through the GIPL

pipeline. Taken together, this infrastructure—combined with ORLEN’s own production—allows Poland to meet domestic demand with a surplus of more than 50%. Additional FSRU capacity will further expand a year, with volumes expected to reach 12 billion cubic meters by the end of the decade. ORLEN also imports gas purchased from external suppliers.

A Regional System Takes Shape

Lithuania has followed a similar path. Its floating LNG terminal in Klaipėda, launched in 2014, gave the country direct access to global markets, strengthening energy independence and increasing price competition. The decision effectively ended decades of Russian monopoly. The terminal’s capacity stands at about 4 billion cubic meters a year. The GIPL interconnector, completed between 2020 and 2022, links Poland and Lithuania and connects the Baltic states to the EU gas system through Poland. It provides access to the Świnoujście terminal and other European sources of supply.

As a result, Lithuania, Latvia, Estonia and Finland are now integrated into the EU transmission network. ORLEN also uses the Klaipėda terminal, and gas has become a connector across markets in the region.

U.S. LNG as a Stabilizing Force

ORLEN has experience trading gas both in Europe and globally, including with markets such as Japan, China, Thailand, and Egypt. It also supplies gas to Ukraine. At the end of 2025, the company signed an agreement with Ukraine’s Naftogaz to deliver more than 300 million cubic meters of U.S.-sourced LNG in the early months of 2026. Total exports to Ukraine this year could reach 1 billion cubic meters.

To maintain flexibility and efficiency in logistics, ORLEN has chartered eight LNG carriers for 10 years, with options to extend. Each vessel can transport about 70,000 tons of LNG, equivalent to roughly 100 million cubic meters of gas. The ships were built in South Korea by Hyundai Heavy Industries and Hanwha Ocean. Each vessel can complete 8–9 voyages annually on the U.S.–Europe route and is equipped with gas re-liquefaction systems and dual-fuel engines capable of operating on both natural gas and diesel.

The United States has become one of Europe’s main LNG suppliers in recent years, particularly after 2022, when Russia lost its position as the continent’s dominant exporter. The expansion of U.S. export capacity and a flexible trading model—based on Free on Board contracts, which allow buyers to redirect cargoes—has made American LNG a key stabilizing factor during supply disruptions.

The scale of U.S. reserves, and their continued growth, means additional volumes can be brought to market as needed, making the U.S. a key source of supply for Europe. The European Union is now the world’s largest LNG importer. The biggest buyers include France, Spain, the Netherlands, Italy, and Belgium. Between 2023 and 2024, LNG import capacity in the EU increased by 70 billion cubic meters, with more than 60 billion cubic meters expected to come online between 2025 and 2030.

A System Built for Resilience

The scale of ORLEN’s operations, combined with Poland’s infrastructure and cross-border connections, positions the country to function as a regional Baltic Eagle Gas Hub for Central and Eastern Europe. The hub is built on a combination of LNG terminals, cross-border interconnectors, storage capacity and a growing fleet of LNG carriers. Together, these elements strengthen the independence of countries in Central and Eastern Europe, reducing exposure to political pressure linked to fuel supplies.

By linking regional markets with global ones, the Baltic Eagle Gas Hub is emerging as part of a new energy-security architecture in Europe—one based not only on diversification of supply, but also on flexibility, regional cooperation and the ability to respond quickly to shifts in the global environment.