Global Nuclear Plant Construction Moves Forward, Except in the U.S. (Politics and market conditions make it tough for a large-scale rival to carbon-based energy)

By Robert Peltier -- November 24, 2009July 17, 1955, was the first time electricity generated by a U.S. nuclear power plant flowed into a utility grid. In what then was an experiment, Utah Power & Light plugged in the Argonne National Laboratory experimental boiler water reactor, BORAX-III.

The plant produced merely 2 megawatts for more than an hour, as planned. Since then, the U.S. nuclear industry has steadily improved their ability to effectively manage the operations and maintenance of nuclear power plants. Now, more than 50 years after that first nuclear power supply, America lags far behind even developing nations in new construction. New roadblocks threaten to further erode progress in the U.S. Whether this is good or not I will leave to the reader, but here is a snap-shot of the situation facing the U.S.

Significant Global Growth

Today, 436 nuclear power plants are in operation in 30 countries with a total capacity of 370 GW, according to the International Atomic Energy Agency (IAEA). The U.S. operates 104 of those plants, totaling a bit over 100 GW of installed capacity. France is runner-up with 59 operating plants and one new plant under construction.

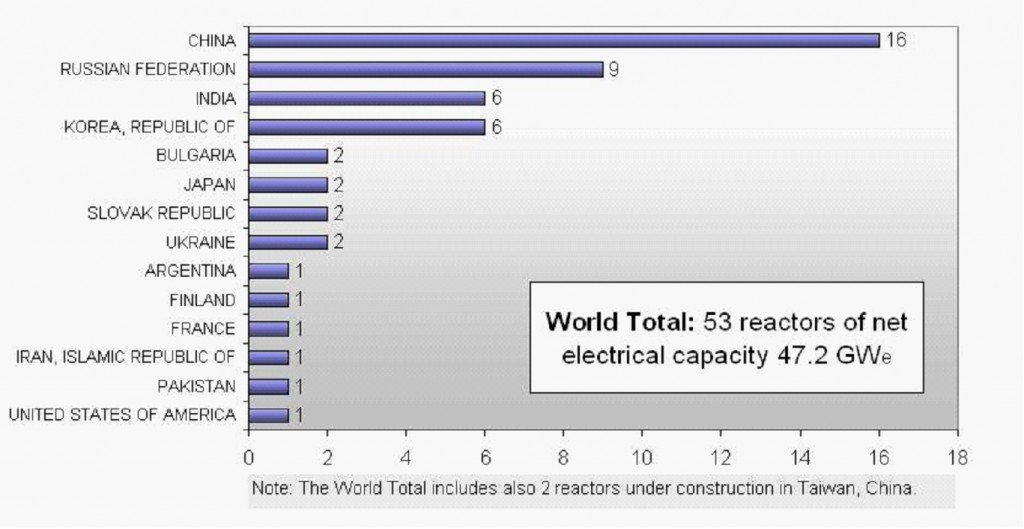

As with picking stocks, the U.S. nuclear industry’s past performance may not be a predictor of future performance. According to IAEA, 53 reactors, rated at just over 47 GW, are under construction around the world today (here). In the U.S., the only “new” nuclear plant is Watts Bar Unit 2. Construction of that unit was stopped in 1985 but restarted two years ago. When completed in 2013, Watts Bar Unit 2 will add almost 1.2 GW to the Tennessee Valley Authority grid (Figure 1).

- Figure 1. The number of reactors under construction worldwide. Source: IAEA

Developing Countries Pick Nuclear

The location of these new reactors provides a peek into where the U.S. fits into the global nuclear marketplace. Unexpectedly, the countries with the largest fleets of operating nuclear plants are not the countries looking to add plants. As many as 20 countries will build nuclear plants by 2030 that do not currently have one.

The numbers also indicate that developing countries are likely to lead the industry in new construction in future years. For example, China, with 11 operating nuclear plants, leads the planet with 16 more under construction. Five of those plants broke ground in 2009 and six in 2008. Next, the Russian Federation, with 31 operating reactors, has another nine reactors under construction. Tied for third place, with six reactors under construction, are India (17 operating reactors) and the Republic of Korea (20 operating reactors). Japan will have 55 nuclear plants when its two units now under construction are completed.

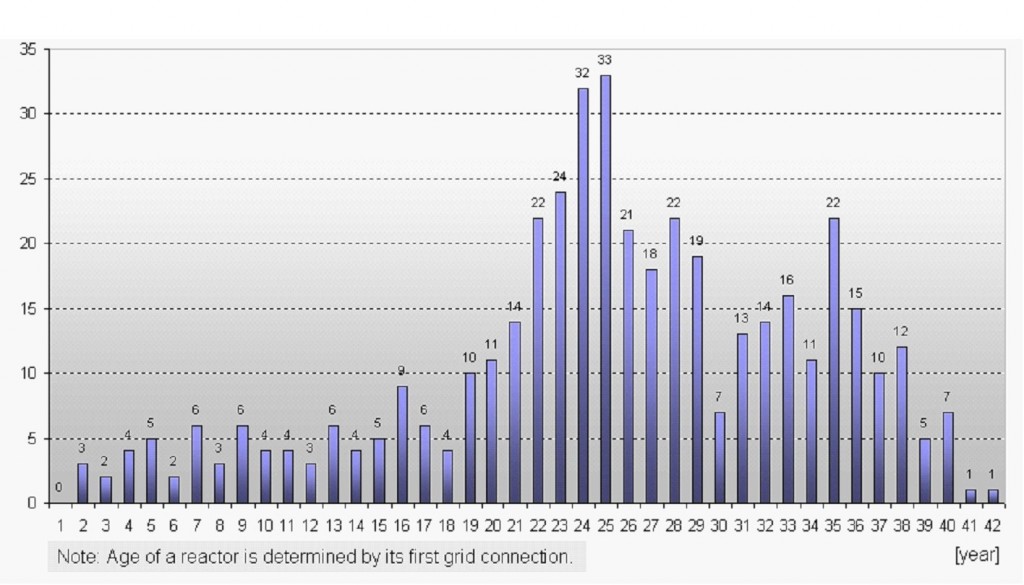

Here’s another interesting observation that helps put the lack of progress of the U.S. nuclear program into perspective. The explosive growth of global nuclear power construction is determined not only by the number of projects under construction but also by the number of projects that have been recently completed. IAEA statistics show that the last nuclear plant to enter commercial service (ignoring the Browns Ferry 1 restart in 2007) was China’s Tianwan 1 and India’s Tarapur 3, both in mid-2006. This fact seems to indicate that there is a growing amount of nuclear work in progress; however, it remains a fraction of the peak of 233 plants in 1979. The average has been around 30 to 40 plants under construction over each of the past 15 years.

Figure 2. The rate of global nuclear plant construction has dropped considerably from its peak in the late 1970’s. Shown are the world’s operating reactors by age, as of March 2009. Source: IAEA

In the November issue of POWER magazine, I predicted–too soon it turns out–that Georgia Power’s plans to add two new AP-1000 reactors to their Plant Vogtle would represent the first wave of new nuclear plants to be constructed in the U.S. (here). The cost of the two units is currently estimated as $14.4 billion. That prediction seemed reasonable as the NRC issued Plant Vogtle an Early Site Permit for its two new units in August and the regulatory climate for nuclear is very good in Georgia. Also, the two new units at Plant Vogtle are the reference plant for the AP-1000 under NuStart making it very likely to be the first licensed installation of the Westinghouse technology. At the time I wrote that article, Plant Vogtle was expecting to begin construction in 2011. Also, the Westinghouse AP-1000 plant design has been identified as the technology of choice by at least 14 possible new plants in the U.S., including six for which the company has signed engineering, procurement, and construction contracts. All-in-all, it seemed like a safe bet.

But it was just after deadline on my article that the roof fell in on the AP-1000. The NRC sent a notice on October 16 to Toshiba Corporation (owner of Westinghouse Electric Co. and the AP-1000 design) that it had not adequately demonstrated the structural strength of certain components of its reactor design, specifically for the shield building. The shield building protects the reactor’s primary containment from severe weather and other events, but it also provides a radiation barrier during normal operation and supports an emergency cooling water tank.

Though the NRC would continue reviewing the remainder of the next-generation reactor’s design certification amendment application, it told Toshiba Corp. that it expected the company to make design modifications and conduct testing to ensure the shield building design could sustain its safety functions.

Then Rep. Ed Markey (D-Mass.) piled on. He suggested that loan guarantees for new nuclear power plants should not be awarded until the NRC has fully reviewed plans for a proposed project and granted it a combined construction and operating license (COL). “Otherwise valuable taxpayer support would be set aside for a project that may not pass regulatory review,” the chair of the House Energy and Environment Subcommittee said in a letter to Energy Secretary Steven Chu.

Markey’s position, given his opposition to nuclear power, was not unexpected but clearly calculated to cause maximum damage to the industry. Chu has not responded to Markey’s letter publically but should Chu adopt Markey’s suggestion, then seven of 17 COL loan guarantee applications that are based on the AP1000 design would be set aside. These include two projects said to be shortlisted for the DOE’s loan guarantees: Southern Co.’s Vogtle plant in Georgia and Scana Corp.’s V.C. Summer plant in South Carolina. The other technologies, including General Electric’s Enhanced Simplified Boiler Water Reactor (ESBWR) and Areva’s Evolutionary Power Reactor (EPR) are several years away from receiving NRC approval. In essence, removing the AP-1000 from the short list of reactors eligible for loan guarantees will push the next new generation of nuclear reactor to be constructed in the U.S. several more years into the future.

Large Market for Nuclear Power Remains Untouched

The U.S. remains the largest single market for new nuclear power plants given its 30-plus applications pending before the Nuclear Regulatory Commission. Nevertheless, the U.S. is also unable to produce pressure vessels and key forgings, it has an unproven new licensing system, it has an administration that seems to be ambivalent about the advantages of nuclear power, and it has a nuclear industry distracted by a potential quick profit from the carbon allowances promised by passage H.R. 2545. The U.S. nuclear industry is producing paper while other countries are pouring concrete.

The Roman poet Ovid is credited with observing that “tempus edax rerum” (“time [is the] devourer of all things”). I hope he wasn’t talking about the nuclear future of the United States. But maybe in the era of superabundant natural gas (not to mention coal supply) nuclear’s renaissance will have to wait until technology and politics combine to create a truly competitive alternative to fossil-fired electricity generation.

As China goes forward with nuclear power, the U.S. fabricates, not nuclear plants, but reasons not to go forward. I had written the following article commenting on this disparity.

ICECAP in the NewsNov 23, 2009

Green Job Benefits – for China By Charles Battig

The October 30, 2009 WSJ edition provides confirmation of the job generating potential of the clean energy revolution so often mentioned by President Obama. Rebecca Smith’s article reports on the new green jobs resulting from the 36,000 acre wind farm in Texas. Unfortunately the jobs are being created in China; I thought that the President was talking about U.S. jobs.

Federal tax credits and millions of dollars of federal funding will be sought to create 2,800 jobs. Great, except that the article notes that the U.S. share of those green jobs would be all of 15%—420 jobs. The other 85% are created in China! The managing partner of the private equity firm behind this project is quoted as calling this a “win-win for everyone.” I say not quite everyone. It is presumably a win for his equity firm and a win for the Chinese turbine manufacturer. The loser in this game would be the U.S. taxpayer, forced to front the costs of this project and pay to ship jobs overseas. Wind power is touted as free, clean energy. Shrewd investors and manufacturers are happy to fulfill this fantasy with taxpayer money. The reported experiences of wind power in Denmark, Germany, and Spain note no closing of coal fired power plants as a result of wind power coming on line. Russian natural gas becomes the alternate back up power source when the wind fails.

Another report in the same WSJ details the Chinese march forward with nuclear powered plants, with plans to have as many as 100 on line in twenty years, up from 11 today. Here in the U.S., nuclear power continues to be hamstrung by environmental groups such as the Sierra Club, and by onerous permitting obstacles. The world’s first AP1000 third generation reactor, pioneered by U.S. Westinghouse, is to be located , not in the U.S., but in China. China is also reported to be the prime manufacturing site for the solar panels used in Germany.

See larger image here.

China has seen the future and it sees that it is jobs and plentiful energy. This is something to remember here as the U.S. Federal energy policy is intent to make energy more expensive via Cap/Tax and Trade legislation. China is happy to fulfill our clean energy fantasies, take our green jobs, while building a new coal power plant each week, and building next-generation nuclear power plants.

Charles Battig, M.S., M.D.

President, Piedmont Chapter

Virginia Scientists and Engineers for Energy and Environment

Charlottesville, VA

A timely article and an excellent comment. I was particularly glad to see the chart showing how committed Russia is to a nuclear future, for I’ve been intrigued with that nation’s recent energy policy. Putin has been pushing nuclear in his country for some time while quietly cheerleading for “renewables” in western Europe, knowing he can increase his energy stranglehold in that part of world, since western European countries would then be even more dependent on Russian natural gas.

This post has been linked for the HOT5 Daily 11/25/2009, at The Unreligious Right

Jon – one of the reasons that Russia is interested in building new nuclear power plants at home is that it would prefer to free up more gas to sell to Europe. It has some excellent marketing people, including the man who originally negotiated the German nuclear phase out – Gerhard Schroder. If Germany had gone through with its plans to shut down its 17 large nuclear power plants, that would have represented a potential gas market of approximately 5 billion cubic feet (170 million cubic meters) per day. In the not too distant past, the selling price for natural gas in Germany was $300 per thousand cubic meters, at that price the natural gas replacement for nuclear power would be a market worth more than $50 million PER DAY!

Funny how much money the US natural gas industry is currently spending to convince lawmakers that gas is newly abundant and that “the future is powered by natural gas”. (I work in Washington and read the buses as they go by.)

Rod Adams

Publisher, Atomic Insights

Host and producer, The Atomic Show

Alternatives like nuclear, which generate significant jobs, taxes and direct as well as secondary spending will strengthen the economies of communities and states. We need significant amount of additional clean and affordable electricity to meet the demand of a growing economy, and nuclear can play a very significant role to acheive this objective

China is not only building the first AP-1000 reactors but is building them CHEAPLY. The first of a kind plants are being built at the cost of about $1.75 billion/GW, and they say they expect to get that down to a cool billion once they get their mass production supply chain in place.

Meanwhile in the USA we have utility companies saying that the exact same design—a US-designed reactor to boot—is going to cost about $5 billion/GW. Why is that? Why can Japan build US-designed ABWRs for $1.4 billion/GW (as they have done) and we have to spend 3X as much in the USA? It’s certainly not because Japan’s labor is cheaper, or because they have native supplies of building materials, or that they have lax regulations (their NRC is patterned after ours).

It’s because our whole system in the US is ridiculously broken, with utility companies building in the insecurity of constructions slowdowns/shutdowns, and generally trying to put in enough padding to compensate for a lack of firm government support (things can change drastically with every administration). England recently changed their laws to ban local communities from stopping nuclear power plant projects once they’ve been approved, a big step in the right direction that, if we emulated them in the USA, could go a long way to bringing costs down.

If we don’t get our act together on this and the other aspects of the industry that encourage cost inflation, we’ll find ourselves buying reactors from the countries that know how to build them for a reasonable price: China, Japan, South Korea (who just got a contract for four reactors from the UAE), even Taiwan.